Debt Ceiling Drama Rubber-Necking

By Peter Tchir of Academy Securities

Rubber Necking

Markets did little last week as bond and stocks seemed to get caught “rubber necking” the Debt Ceiling “drama” for lack of a better word. 2-year treasuries moved a few bps higher, along with a slightly increased probability of a hike at the next meeting. The 10-year, the S&P 500 and Nasdaq barely budged on the week, as Debt Ceiling discussions sucked up all of the oxygen.

The “interesting” part is that despite all the Debt Ceiling chatter and analysis, virtually no one thinks we will default. So why all the rubber necking? Unless, just maybe, there is a nagging doubt that this time around, the “inevitable” passing of legislation raise the debt ceiling, could run into complications.

We discuss this, and our thoughts on how any default might play out, in Debt Shilling. We also got to discuss this subject, the issues facing banks and the transition from Made in China to Made by China on Bloomberg TV on Friday.

While I hope the U.S. does not default, the CDS market is pricing in around a 5% chance, which may even be low. In any case, if we do default, I hope it is on June 16th, as Academy will be a guest host from 6 am to 7 am on Bloomberg Surveillance that morning, and it would make for one heck of a show!

On the other hand, maybe we make some progress, and we can stop the rubber necking and move on to what major theme will drive markets and the economy next.

CONsumer CONfidence was the Anti-Goldilocks

CONsumer CONfidence has never been a report I take a lot of stock in (from 2021). More often than not it seems to track some combination of the S&P 500 (for conditions) and gas prices (for inflation).

Friday’s numbers were quite interesting as sentiment plummeted (57.7 was a drop from 63 and pulls us back to levels from last autumn). Current conditions and expectations also fell, continuing a trend. Given the historical correlations with the equity market, that move was a bit surprising.

On the other side of the coin, 1-year inflation expectations remain at 4.5% (well above where the Fed would like to see them) and the longer dated inflation expectations increased to 3.2%. The last time expectations for 5-10 year inflation was that high was back in May 2008!

This data is quite literally the anit-Goldilocks. Rising inflation with weak growth has a name – stagflation. While there were far too many mentions of stagflation on Friday, for my tastes, it does seem to fit a theme of an economy that is weakening while many continue to raise prices on almost anything they can. Danger Will Robinson.

Again, CONsumer CONfidence isn’t something I rely on, but this one caught my eye, because it spun a negative story (and I remain bearish, so who doesn’t love some confirmation bias), but because it wasn’t accompanied by lower stock prices and higher energy prices, which likely means something.

Life Nor Markets Are Like a Video Game

Last weekend, we cautioned that the market seemed to be in a mood where we can “solve” complex issues in a very short period. That we could find and solve a “banking crisis” in a week was just one example raised in Life in a Video Game.

Last week (I think it was just last week, though it seems like longer), the market was focused on the SLOOS report, which I can readily admit, is one of the few times I can remember anyone even mentioning SLOOS, let alone focusing on it as a potential market moving event.

The most important part of that report, from my perspective, was the decline in loan demand.

Sure, the willingness to lend might be shrinking, but there are alternatives to borrowing from banks. The drop in demand for lending seems more problematic as it reflects companies (and individuals) seeing either a smaller opportunity sets or increasing concern about their ability to pay off such debt.

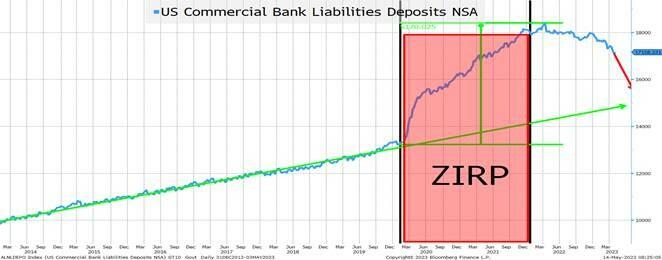

Ultimately, I still think this is the most important chart for the banking sector. (please see I Know what You Did Last Summer, for more analysis in this vein).

Banks deposits grew at a steady pace of $500 billion a year. Then in less than 2 years, banks took in $5 trillion. While that could be a positive, it came during the midst of ZIRP (large scale asset purchases (or QE), low interest rates, stimulus up the wazoo, etc.).

This flood of deposit money came during a period of extremely low yields.

It should surprise absolutely no one, that some institutions would make bad decisions when it came to navigating the 5 Circles of Bond Investor Hell.

Banks, like any other investor base, will behave on a continuum, with some chasing yield and NIM by taking on excessive risk, while others would be more cautious and patient.

The risk, as I see it, is that as banks that made the worst decisions have their portfolios scrutinized, it lowers prices, potentially shining a light on the next level of least prudent investors. The “tail risk” is that occurring which we tease in “Mommy, Where Do Bond Losses Come From?” which is all about forced selling and almost nothing about default.

This will take time to play out and will be a headwind of markets and the economy!

China and the Yuan

We are having more and more conversations about China where “Reserve Currency” is addressed.

This does warrant a full T-Report, which will come later this week, as I’m on the road seeing a lot of clients with multiple members of Academy’s Geopolitical Intelligence Group.

Ahead of those meetings we can make three quick statements (some of which were highlighted in Locking in Some Themes and were discussed in our “China’s Increasing D.I.M.E. Prowess” webinar.

The “Re-opening”. Overhyped as China didn’t go from 0 to 100, more like 70-90. Also, China’s focus is increasingly domestic focused and working with the resource rich nations of the world, limiting the impact on the global economy.

From Made In China to Made by China. Increasingly look for China to exercise their levers of power (primarily Diplomatic and Economic) to shift from merely being the manufacturing hub for goods made on behalf of multi-national corporations to trying to make goods to sell on behalf of China Inc. (for lack of a better word, since it is difficult to separate the country from the companies).

More Like a “Dark Web” than Reserve Currency. I don’t see the status of the dollar as the world’s reserve currency as being threatened, but more trade will occur outside of the dollar sphere of influence and some countries will shift to a system that gives the yuan some elements of reserve currency. Increasingly, I’m concerned that I’m too sanguine on this matter. China is showing great skill at starting to “roll up” some of the weaker global players and I can’t help but frame this in military terms. While they may not be close to launching a frontal assault, they are taking out some units that may let them outflank us, if we are not careful.

Bottom Line

Still bearish on credit and equities on a -4 out of a scale of -10 to 10. Largely neutral on rates, in a relative on rates, though there is potentially increased risk of a short squeeze.

The “new” thoughts are:

Don’t expect a big relief rally from stocks if the debt ceiling is raised without too much pain as, for all the chatter, little actual fear is priced in.

If you need to issue debt, issue now. Summer and the debt ceiling will likely dry up liquidity at least for a few weeks at the start of the summer.

Happy Mother’s Day and celebrate friends and family today, but remember, we should really celebrate friends and family every day!

Tyler Durden

Sun, 05/14/2023 – 12:30