Walmart Beats Across The Board, Boosts Guidance But Warns of Spending Softness As Quarter Progressed

Earnings season came to a soft close this morning when the last big retailer, Walmart, reported earnings and comp sales that were stronger than expected across the board, and also hiked its full year guidance even as it echoed Target in warning that sales have moderated as the quarter progressed with general merchandise sales reflected softness in discretionary categories including home, electronics and apparel.

Starting at the top, this is what WMT reported for Q1:

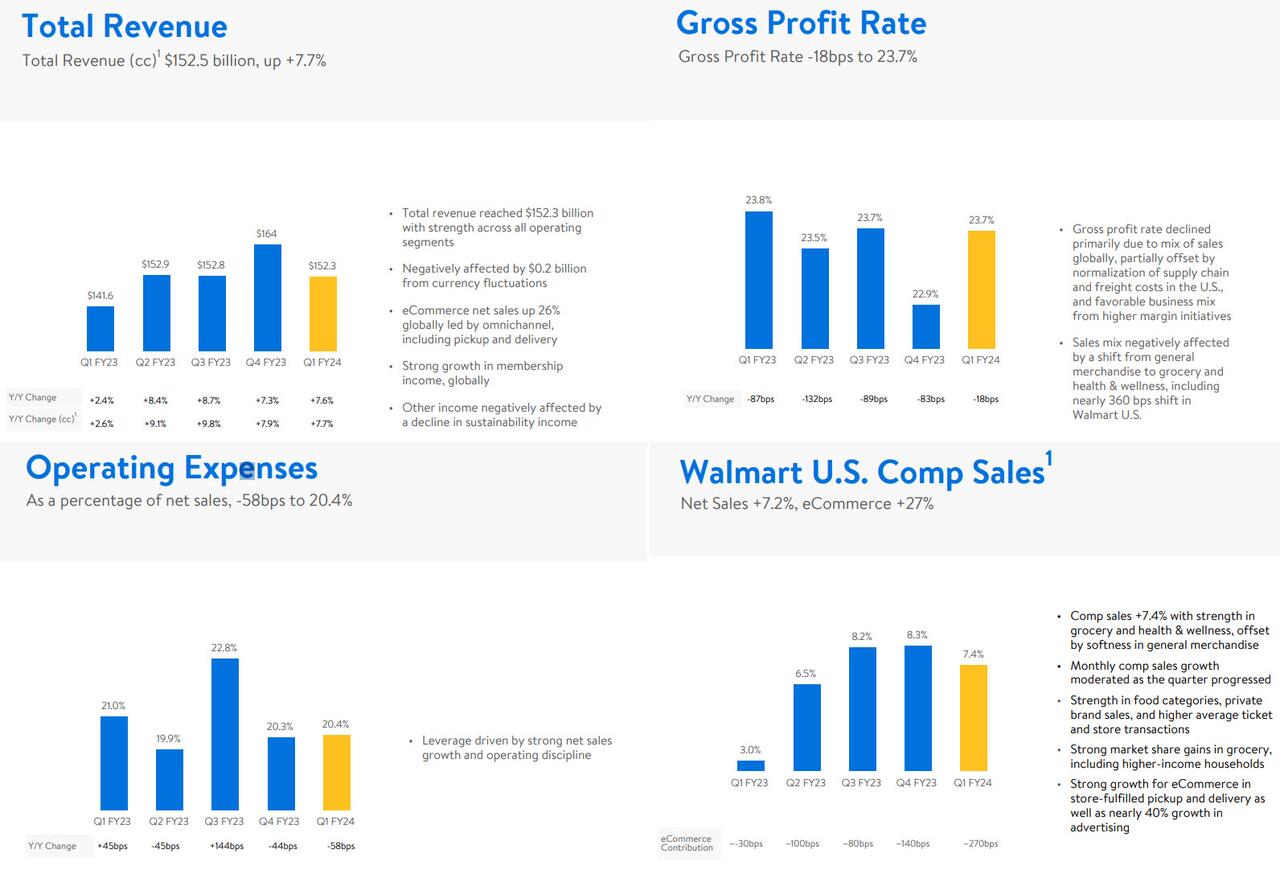

- Revenue $152.30 billion, +7.7% y/y, beating estimates of $148.72 billion, with “strength across all operating segments; Negatively affected by $0.2 billion from currency fluctuations”, and while there was “strong growth in membership income”, “other income was negatively affected by a decline in sustainability income”

- Adjusted EPS $1.47 vs. $1.30 y/y, beating estimates of $1.31

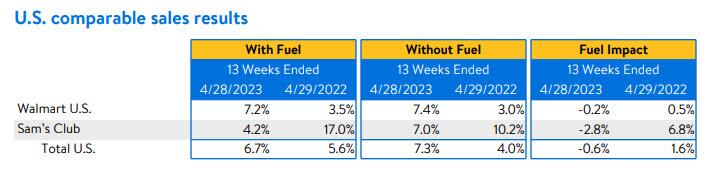

- Total US comparable sales ex-gas +7.3%, beating the estimate +5.08%

- Walmart- only US stores comparable sales ex-gas +7.4%, beating estimates of +5.23%, with strength in grocery and health & wellness, offset by softness in general merchandise

- Sam’s Club US comparable sales ex-gas +7%, beating estimates of +6.81%, driven by “increases in ticket and transactions as well as unit growth”

- Walmart eCommerce net sales up 26% “led by omnichannel, including pickup and delivery”

- Change in Sam’s Club e-commerce sales +19%, missing estimates of +19.8% (2 estimates)

- Gross profit rate declined to 23.7% from 23.8% “primarily due to mix of sales globally, partially offset by normalization of supply chain and freight costs in the U.S., and favorable business mix from higher margin initiatives.” Additionally, “the sales mix negatively affected by a shift from general merchandise to grocery and health & wellness, including nearly 360 bps shift in Walmart U.S.”

- Operating cash flow increased to $4.6BN from a burn of ($3.8BN) “due to moderated levels of inventory purchases and timing of certain payments”

- Free cash flow also increased to $0.2BN from a burn if ($7.3BN) “due to the improvement in operating cash flow, partially offset by an increase of $0.9B in capital expenditures to support the company’s growth strategy”

With comp sales easily topped Wall Street’s estimates, even as Walmart said shoppers will remain under pressure this year, CFO John David Rainey said that strong demand spurred higher-than-expected earnings in the first quarter, fueling the increase in the company’s outlook.

“There’s reason to be somewhat cautious on the health of the consumer, but if you look at our results in the quarter, it certainly speaks to our value proposition resonating with customers,” Rainey said in an interview. “The outlook on the rest of the year hasn’t changed appreciably.”

The upbeat results point to the resilience of Walmart’s massive grocery business, which is enabling the company to grab more sales even as US shoppers think twice before buying discretionary goods. Target warned of softening sales trends this week, while Home Depot cited a consumer pullback in cutting its annual profit forecast.

And speaking of guidance, looking ahead Walmart boosted its adjusted earnings per share forecast for the full year, which is now in line with Wall Street consensus even if the company’s Q2 guidance came in modestly short of expectations:

Second Quarter Forecast

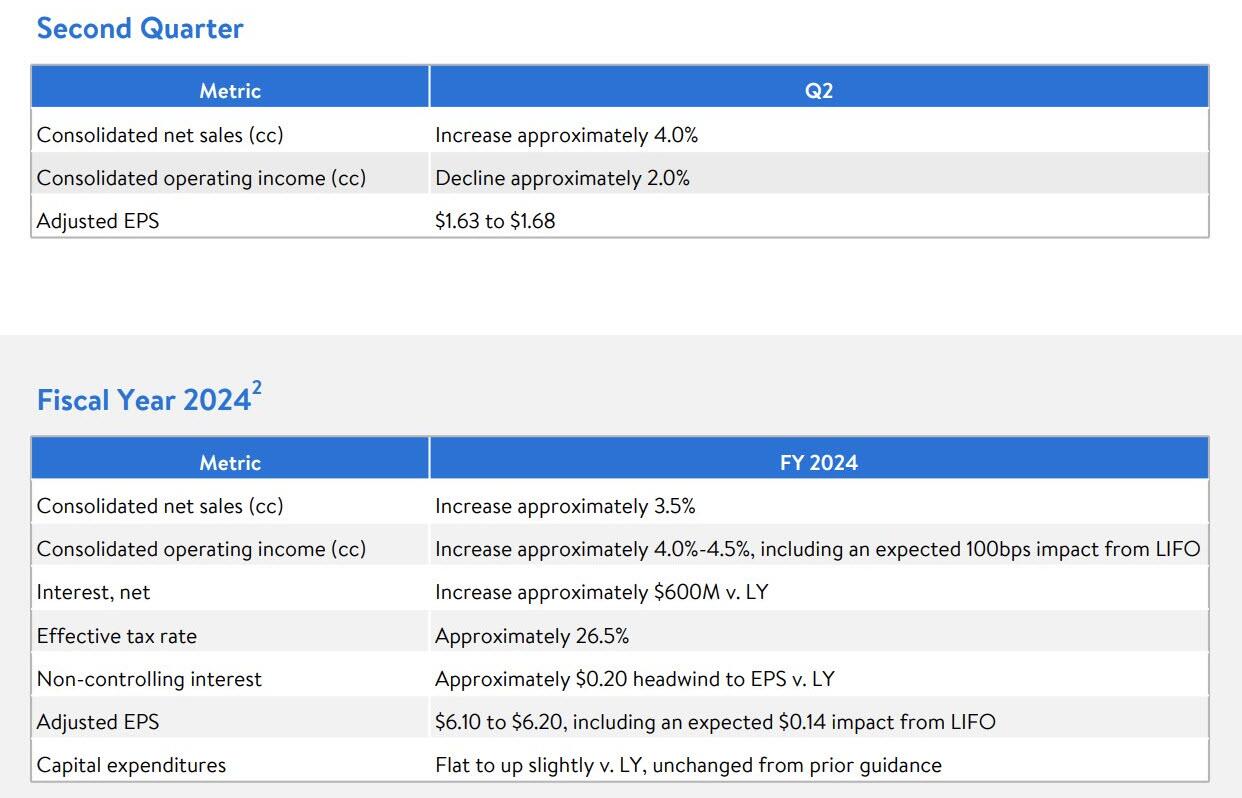

- Sees adjusted EPS $1.63 to $1.68, both below the estimate $1.70

- Sees consolidated net sales up about 4%

- Sees consolidated operating income decline about 2%

Full Year Forecast

- Sees adjusted EPS $6.10 to $6.20, previously saw $5.90 to $6.05, the mid-point coming above the estimate of $6.14

- Sees net sales +3.5%, previously saw +2.5% to +3%

- Sees year consolidated operating income increase approximately 4.0%-4.5%, including an expected 100bps impact from LIFO

- See year capital expenditures flat to up slightly, unchanged from prior guidance

In short, according to the company “expectations are for Walmart U.S. and International to grow slightly faster than our prior view and for Sam’s Club growth to be consistent with our February guidance.”

Commenting on the quarter, CEO Doug McMillon said “We had a strong quarter. Comp sales were strong globally with eCommerce up 26%. We leveraged expenses, expanded operating margin, and grew profit ahead of sales.”

The CEO also touched on inflation which “remained high, up low double digits and food categories…On a two-year stack basis, food inflation remains over 20% and continues to pressure discretionary wallets.”

However, while results were generally solid, the company issued a warning which echoes what both Target and we observed previously, namely that there has been a slowdown in spending in recent weeks: the company said that US monthly comp sales growth moderated as the quarter progressed and general merchandise sales reflected softness in discretionary categories, including home, electronics, and apparel. One can only assume that the March weakness spilled over into April and May.

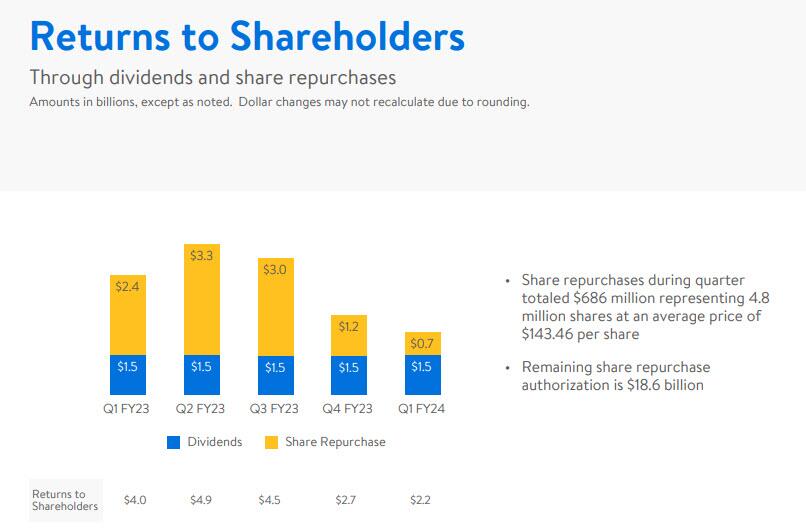

Separately, WMT said it repurchased 4.8 million shares, returning $0.7 billion to shareholders; and advised that it has $18.6 billion remaining of its latest $20 billion authorization approved in November 2022.

WMT shares rose 3% at the open of trading; Walmart climbed 5.5% this year through Wednesday, trailing the S&P 500 index’s 8.3% gain.

Walmart’s full Q1 earnings presentation below (pdf link)

Tyler Durden

Thu, 05/18/2023 – 09:34