Are You Ready For A Real Recession?

Authored by Charles Hugh Smith via OfTwoMinds blog,

In a real recession, what seemed safe and rock-solid melts into air.

We haven’t had a real recession in forty years (1981-82) and so only those who were in the workforce back then have any experience of how far and how fast things we think are solid can unravel. What’s a real recession? In the most basic terms, a real recession is an organic, i.e. unmanipulated by central banks, completion of the credit cycle, also known as the business cycle.

The credit / business cycle is intuitively easy to understand. When the cost of borrowing money (a.k.a. the cost of capital) declines and credit standards loosen so more enterprises and households can qualify for loans, the incentives to borrow and spend / expand increase. Lenders start making more money because they’re lending more, and borrowers expand their enterprise, buy assets such as bigger homes and retailers sell more goods and services to borrowers who can now access new sources of credit–home equity lines of credit, higher credit card limits, etc.

All of this credit expansion is self-reinforcing. Free-spending consumers boost sales and profits, lenders are expanding as borrowing soars, enterprises expand to meet new demand, and so on.

Then diminishing returns set in. To maintain the gushing river of profits from expanding credit, lenders loosen standards to the point that marginal enterprises, speculations and households all have access to low-cost credit. Since asset prices skyrocketed as credit pushed demand higher, new investments are increasingly at risk of becoming unprofitable. Those who overborrowed are increasingly at risk of defaulting should their income slip even slightly.

Eventually, those who were poor credit risks to start with overborrow and invest in marginal speculations that collapse. These marginal borrowers default, and eventually lenders are forced by the losses to tighten lending standards. This reduces the number of people who qualify for additional credit, and the credit river dwindles to a rivulet.

The wealthy who can still borrow have no desire to add more debt, and those desperate to borrow more no longer qualify to add more debt. (If you’re old enough, you might have heard the expression “Prove you don’t need the money and then the bank will lend it to you.”)

The self-reinforcing expansive cycle turns to self-reinforcing contraction. Lending, consumption, investment and speculation all drop, reinforcing the contraction, a.k.a. recession.

The organic credit cycle is self-clearing: the analogy of the forest fire is apt. All the dead wood of marginal loans and speculations are consumed–that is, marginal debtors default and unpayable debt is written down as losses–and this destruction of bad debt is necessary to clear the financial system and economy for the next growth cycle.

The Federal Reserve has unleashed floods of “free money” every time the credit cycle started its cleansing phase for the past three decades, effectively eliminating the essential writedowns of bad debt and the tightening of credit that set the stage for organic growth, i.e. growth that isn’t the result of stimulus extremes such as Zero Interest rate Policy (ZIRP).

Now four dynamics will usher in the long-suppressed real recession conflagration:

1. Diminishing returns on fiscal and monetary stimulus and the easing of credit. Every cycle of Fed largesse yields weaker, narrower growth and exacerbates wealth-income inequality.

2. Inflation is sticky due to fundamental scarcities and structural changes in the global economy. The global economy, demographics and the cost of capital have all changed. Locking interest rates at zero for another 15 years is no longer a viable “fix.”

3. Higher interest rates undermine speculation and the asset-bubble dependent economy. Since rates can’t be locked down at zero, a truly stupendous quantity of speculative skims and scams are no longer low-risk or profitable. As these skims and scams unravel or go belly-up, they self-reinforce the decay and collapse of all other debt-based skims and scams.

4. Cheap credit has raised costs. High fixed costs push households, enterprises and governments into insolvency. When credit is abundant and cheap, there’s little pushback against higher prices: just borrow more. Once credit contracts and the cost rises, borrowing more is no longer an option. The only remaining option is default and insolvency on a mass scale.

As I noted last week, our collective response is now limited to either 1. complacency / denial or 2. panic. We’re still anchored in complacency / denial, but the phase shift to panic is just around the next corner.

In a real recession, growth doesn’t dip slightly for a few months. It drops for years. In a real recession, employment doesn’t dip for a quarter or two, it plummets hard and keeps dropping, quarter after quarter. In a real recession, borrowing doesn’t dip for a quarter, it goes downhill for years. In a real recession, spending and consumption don’t dip for a few months, they fall off a cliff and then stumble further down the ravine.

In a real recession, the Fed’s tricks no longer work. Fiscal stimulus is limited by the overborrowing of the previous decades of inorganic (i.e. credit-dependent) “growth.”

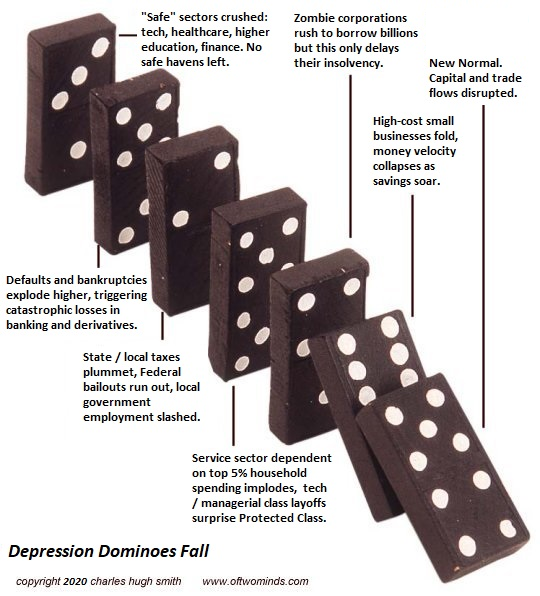

In a real recession, the dominoes fall regardless of what policy tweaks are rushed into place. This is what happens when you let the dead wood and risk pile up. Eventually you can no longer suppress the conflagration.

In a real recession, what seemed safe and rock-solid melts into air. Jobs, income, tax revenues and much else that sre seen as utterly dependable will evaporate. One week your bosses tell you how much they love your work and the next week you’re cashiered or the whole business is shuttered. Assets that “never go down” don’t just go down, they fall in half. And so on.

The solution for households and small enterprise is to change course now and seek to reduce risk and exposure to conflagration. I call this process improving our Self-Reliance.

* * *

My new book is now available at a 10% discount ($8.95 ebook, $18 print): Self-Reliance in the 21st Century. Read the first chapter for free (PDF)

Tyler Durden

Tue, 05/23/2023 – 12:25