US Futures Leap Led By Report-Breaking Surge In Nvidia

US fairness futures are increased led by tech names after blowout earnings reported by Nvidia – which as Goldman reminds us “is now #5 weight within the S&P and the poster baby for “AI” Euphoria + momentum” – whose inventory is up virtually 30% premarket and quickly approaching $1 trillion in market cap. S&P futures had been up 0.6% to 4,151 with Nasdaq 100 futures up a whopping 2% led increased by NVDA and semi shares. Bond yields are barely increased, whereas USD is stronger. Commodities are principally decrease as WTI fell 1.5% reversing all of yesterday’s features after Russia performed down the probability of OPEC+ reducing manufacturing additional.

In premarket buying and selling, Tech shares are surging boosted by NVDA which reported after the bell yesterday with forecast beat; shares is up virtually 30% after shut. For some context, NVDA added > $200bn in market cap in a single day publish earnings and as Goldman notes, “this could be the most effective TMT earnings print we have seen since that June qtr 2020 print from Zoom (ZM), once they beat revs by ~62%.” In any case, it’s one other signal that traders are keen to pile into promising tech shares, regardless of the rising worries about China’s financial system and a doubtlessly catastrophic US debt default.

“In the event you take a look at tech it continues to reinvent itself again and again,” Larry Adam, chief funding officer at Raymond James, stated in an interview on Bloomberg Tv. “I proceed to love the massive tech names.”

Listed here are another notable premarket movers:

- American Eagle Outfitters (AEO) shares tumble 21% after the attire retailer’s forecast for the full-year upset analysts.

- Carnival Corp. (CCL) rises 2.5% after Citi upgrades to purchase from maintain, citing in word continued good momentum for the cruise sector.

- Desktop Metallic (DM) shares commerce 9.1% increased after Stratasys agreed to purchase the 3D printer firm in an all-stock transaction valued at round $1.8 billion. Stratasys shares are up 3.8%, reversing an earlier drop.

- Dish Community Corp. (DISH) shares are down 3.4% after Citi downgraded the satellite tv for pc tv firm to impartial from purchase.

- Dorian LPG (LPG) upgraded to outperform from inline at Evercore ISI based mostly on valuation, following the propane fuel shipper’s fourth-quarter outcomes. Shares are up 1.1%

- Dycom Industries (DY) rises 1.5% as Wells Fargo raises to chubby from equal-weight after the engineering providers firm “massively” beat first-quarter expectations.

- Leidos (LDOS) rises 1.7% after Wells Fargo upgrades to chubby from equal-weight, saying the engineering firm’s valuation consists of an excessive amount of worry round short-term uncertainty, whereas not making an allowance for upside for 2024 gross sales, margin and money movement.

- Nutanix (NTNX) shares are up 17% after the infrastructure-software firm boosted its income steerage for the complete 12 months. The outlook beat the typical analyst estimate. The corporate additionally stated its audit committee accomplished an investigation of third-party software program utilization.

- Nvidia Corp.’s (NVDA) blowout gross sales forecast places a contemporary emphasis on the most recent sport on the town: figuring out synthetic intelligence losers. Shares are up 28%.

- Snowflake (SNOW) shares fall 13% after the cloud-software firm reduce its product income steerage for the complete 12 months.

In different in a single day information, Fitch put US’s AAA score on detrimental watch amid debt ceiling considerations, and this morning DBRS echoed the transfer when it “Placed United States Ratings Under Review With Negative Implications.” McCarthy signaled some progress being made on the negotiation, however representatives will not be required to remain in DC over the vacation weekend. In the meantime, JPM sees the percentages of passing x-date with out a rise within the ceiling index is now round 25% and rising.

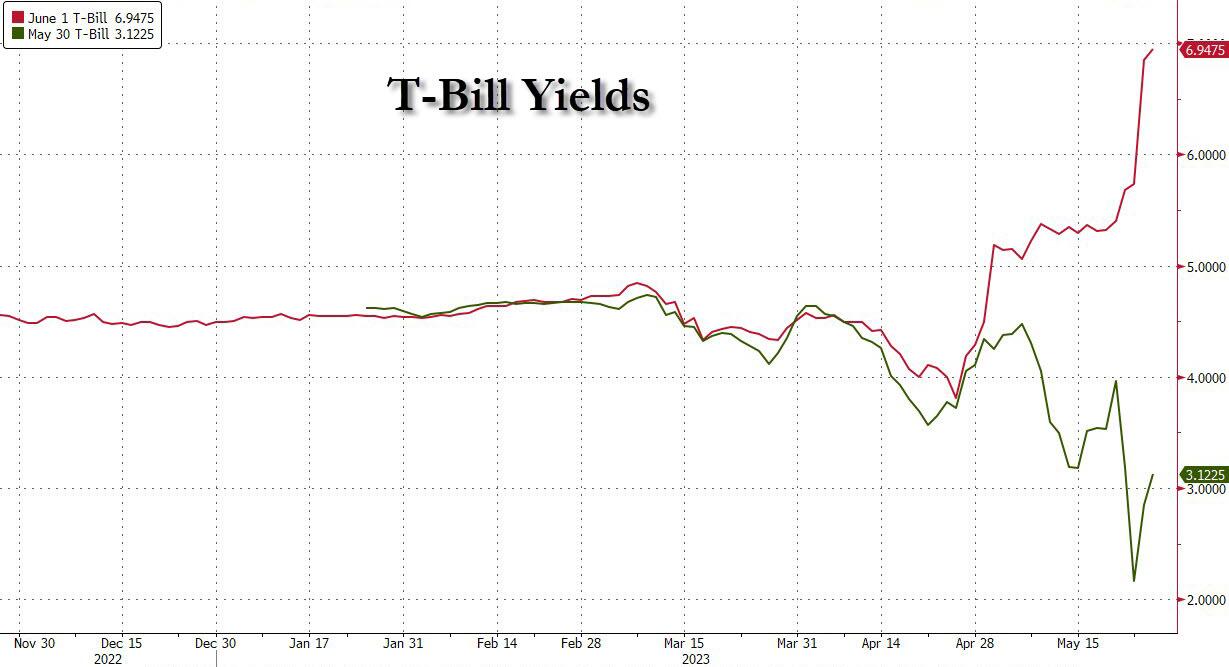

Elsewhere, Treasury-bill yields slated to mature early subsequent month surged above 7% on Wednesday, with the speed on the June 1 and June 6 maturities growing by greater than a proportion level. These securities are seen as most vulnerable to non-payment if the federal government exhausts its borrowing capability. On Thursday morning, Payments maturing on June 1 traded simply round 7%.

“Nvidia was final night time’s good shock,” stated Gilles Guibout, head of European fairness methods at Axa Funding Managers. “However extra broadly, there are few causes for the market to maintain rising: rates of interest will not be happening, international financial progress isn’t rebounding, full-year earnings are seen flat and inventory valuations are already at a good stage.”

European markets had been propped up by chipmakers after gross sales steerage from Nvidia smashed expectations – shares within the US semiconductor maker are up ~28% within the premarket. The Stoxx 600 is up 0.1% after touching a seven-week low on Wednesday. Listed here are among the most notable European movers:

- ASML leads a rally in shares of European semiconductor tools makers after US chipmaker Nvidia gave a gross sales forecast that blew previous estimates, boosted by burgeoning AI demand

- GN Retailer Nord features as a lot as 10%, probably the most in a month, after a DKK2.75 billion rights concern removes a “important overhang” for the Danish hearing-aid and audio tools agency, Citi says

- Tate & Lyle rises as a lot as 2.6% after the elements firm reported FY23 outcomes and forecast income progress of 4%-6% for the present fiscal 12 months. The revenue beat was spectacular, Citi says

- Elekta shares acquire as a lot as 4.8% after the Swedish medical know-how agency beat expectations on gross sales and Ebit, with Handelsbanken noting the corporate’s free money flows are at a file excessive

- D’Ieteren rises as a lot as 3.3% after the automotive retailer reiterates its pretax revenue steerage for the complete 12 months. Analysts flag this was maintained regardless of prices related to current refinancing

- QinetiQ rises as a lot as 2.2%, snapping three days of declines, after the British know-how and analysis agency delivered full-year outcomes that Barclays says beat consensus on all metrics

- ALSO features as a lot as 2.4% after Stifel initiated protection of the Swiss IT and client electronics wholesaler with purchase, saying its cloud market enterprise is an underestimated worth driver

- Allegro shares fall as a lot as 6.7%, their largest decline in additional than 4 months, after Poland’s largest e-commerce platform guided for slower gross merchandise worth progress in 2Q

- Johnson Matthey shares decline as a lot as 3.8%, to the bottom since October, after the UK-based chemical substances firm revealed below-consensus steerage for this 12 months and subsequent

Earlier within the session, Asian shares had been principally decrease with the area cautious after the losses on Wall Avenue as a result of debt ceiling fears. The MSCI Asia-Pacific index closed 0.8% decrease for the day as sentiment round Chinese language markets continued to worsen. The Hold Seng Index shed 1.9% on the day and the yuan broke by means of the closely-watched 7-per-dollar stage. The important thing fear for traders is that China’s financial system is dropping momentum and there are persistent monetary troubles in the true property trade. Current knowledge recommend gross home product progress this 12 months will likely be nearer to the federal government’s goal of about 5%, opposite to expectations of a big overshoot fashioned earlier within the 12 months. The Hold Seng was pressured with underperformance in Hong Kong after the benchmark index slipped beneath the 19,000 stage.

- Japan’s Nikkei 225 was saved afloat however with the upside capped within the absence of any main constructive drivers.

- Australia’s ASX 200 weakened because the commodity-related sectors led the broad declines throughout almost all industries and with sentiment additionally dampened as households are set to pay a whole lot of {dollars} extra annually after the vitality regulator authorized a rise of as much as 25% in electrical energy payments.

- Korea’s KOSPI was subdued after the BoK charge resolution wherein the central financial institution saved charges unchanged as anticipated, though 6 out of the 7 board members noticed the necessity to hold the door open for yet one more charge hike.

- Indian shares recovered late within the day to finish increased and outperform most of their Asian friends whilst broad sentiment stays cautious amid ongoing considerations of a doable debt default by the US. The S&P BSE Sensex rose 0.2% to 61,872.62 in Mumbai, whereas the NSE Nifty 50 Index superior 0.2% to 18,321.15. Shares of client staple, vitality and communication providers companies, a part of the benchmarks, led the restoration because the Might futures contract expired.

In FX, the Bloomberg greenback index climbed for a fourth day, boosted by rising US yields and more-averse buying and selling circumstances after Fitch Scores on Wednesday stated it could downgrade the US’s AAA credit standing; the kiwi is the weakest of the G-10 currencies. The USD/JPY was little modified at 139.49, holding close to 139.70 hit in earlier commerce, its highest since late November.

In charges, treasuries are decrease with the US 10-year yield rising 1bps to three.76% forward of GDP and claims knowledge. The yield on two-year Treasuries rose 4 foundation factors to 4.42%, its highest since March; merchants are pricing in an almost 50% probability that the Fed will elevate charges by 25 foundation factors subsequent month; 10-year yields sit round 3.76%, with gilts buying and selling cheaper by 10bp within the sector as rate-hike premium will increase additional in sterling swaps. A late Wednesday announcement that Fitch positioned US credit score on “score watch detrimental” elicited restricted market response. The US public sale cycle concludes with $35b 7-year word sale at 1pm, following sturdy demand for 2- and 5-year gross sales. WI yield round 3.790% is ~25bp cheaper than final month’s, which tailed by 1.3bp.

In the meantime, UK authorities bonds led losses in Europe. Merchants added to bets the Financial institution of England will hold elevating rates of interest after an unexpectedly sturdy studying of UK inflation Wednesday. Cash markets at the moment are pricing greater than 100 foundation factors of further tightening by December.

In commodities, WTI declined 1.3% to commerce close to $73.40 on Thursday after the greenback strengthened and Russia performed down the probability of OPEC+ reducing manufacturing additional. Billionaire mining investor Robert Friedland says the copper market weak point is momentary. Southwestern Power is among the many most energetic assets shares in premarket buying and selling, falling 4.6%.

Bitcoin is decrease however holding above the $26k mark regardless of briefly dropping beneath in early commerce, with the USD capping upside and broader marks nonetheless centered on the debt ceiling as we close to the US lengthy weekend.

To the day forward now, and knowledge releases from the US embody the weekly preliminary jobless claims, the second estimate of Q1 GDP, pending residence gross sales for April, and the Kansas Metropolis Fed’s manufacturing index for Might. Central financial institution audio system embody the Fed’s Barkin and Collins, ECB Vice President de Guindos and the ECB’s Nagel, Villeroy, Centeno and De Cos, together with the BoE’s Haskel.

Market Snapshot

- S&P 500 futures up 0.5% to 4,144.75

- MXAP down 0.8% to 159.34

- MXAPJ down 0.9% to 503.86

- Nikkei up 0.4% to 30,801.13

- Topix down 0.3% to 2,146.15

- Hold Seng Index down 1.9% to 18,746.92

- Shanghai Composite down 0.1% to three,201.26

- Sensex down 0.4% to 61,526.09

- Australia S&P/ASX 200 down 1.0% to 7,138.16

- Kospi down 0.5% to 2,554.69

- STOXX Europe 600 down 0.1% to 457.06

- German 10Y yield little modified at 2.47%

- Euro down 0.2% to $1.0727

- Brent Futures down 0.9% to $77.68/bbl

- Gold spot up 0.4% to $1,964.02

- U.S. Greenback Index up 0.16% to 104.06

High In a single day Information

- China’s muted financial rebound and Beijing’s reluctance to deploy large-scale stimulus are reverberating across the globe, crushing commodity costs and weakening fairness markets. Buyers are pegging again their expectations for the world’s second-biggest financial system as worries mount that its restoration from pandemic restrictions has misplaced momentum. BBG

- The widening rift between the world’s two largest economies, the US and China, now seems in some regards to be irreconcilable, in keeping with Singapore Deputy Prime Minister Lawrence Wong. The geopolitical state of affairs has turn out to be extra harmful amid tensions between the 2 sides with the Taiwan Strait changing into the area’s “most harmful flashpoint,” Wong stated in his speech on the Nikkei Discussion board twenty eighth Way forward for Asia in Tokyo. BBG

- Russian Deputy Prime Minister Alexander Novak stated on Thursday he anticipated no new steps from the OPEC+ group of oil producers at its assembly in Vienna on June 4, Russian media reported, after the group introduced a big output reduce earlier this 12 months. RTRS

- Germany suffered its first recession because the begin of pandemic, extinguishing hopes that Europe’s prime financial system may escape such a destiny after the battle in Ukraine despatched vitality costs hovering. First-quarter output shrank 0.3% from the earlier three months following a 0.5% drop between October and December, the statistics workplace stated Thursday. Its preliminary estimate, final month, was for stagnation. BBG

- Do not anticipate Fed charge cuts till “effectively into 2024,” Raphael Bostic warned. “The tightening that we have achieved is simply beginning to present up,” nevertheless it’s not clear how a lot time it’s going to take for increased charges to sluggish the financial system. BBG

- Fitch Scores is reviewing whether or not the U.S. ought to retain its prime credit standing because the White Home and Republicans battle to achieve an settlement on elevating the debt restrict. WSJ

- On Friday, June 2, hundreds of thousands of People are due a complete of $25 billion value of Social Safety funds. And greater than anything, that will show a decisive ingredient in forcing an finish to the partisan standoff over elevating the federal debt restrict. That obligation is “an enforcement mechanism we are able to’t ignore,” Democratic Senator Chris Coons of Delaware, one in every of President Joe Biden’s prime allies in Congress, stated on MSNBC Wednesday. “After they discover out that they’re not getting that examine, our telephones will gentle up like a Christmas tree.” BBG

- Richard Branson’s Virgin Galactic faces an important take a look at of whether or not it may well begin its business house service subsequent month. Unity 25, scheduled to carry off at 8 a.m. native time from New Mexico, will take a six-person crew to the sting of outer house. It is solely been to house 4 occasions and has suffered technical points throughout flights and a crash in 2014. The corporate, which had anticipated to start out business service on the finish of 2022, additionally should overcome doubts about its monetary viability. BBG

- NVDA added > $200bn in market cap in a single day publish earnings. Hardly any ‘actual’ suggestions from traders, however this could be the most effective TMT earnings print we have seen since that June qtr 2020 print from Zoom (ZM), once they beat revs by ~62%

A extra detailed take a look at international markets courtesy of Newsquawk

Asia-Pac shares had been principally decrease with the area cautious after the losses on Wall St owing to debt ceiling fears and after the FOMC Minutes confirmed officers had been cut up on help for extra hikes, whereas Fitch positioned the US AAA sovereign score on Ranking Watch Damaging regardless of a number of optimistic feedback from Home Speaker McCarthy. ASX 200 weakened because the commodity-related sectors led the broad declines throughout almost all industries and with sentiment additionally dampened as households are set to pay a whole lot of {dollars} extra annually after the vitality regulator authorized a rise of as much as 25% in electrical energy payments. Nikkei 225 was saved afloat however with the upside capped within the absence of any main constructive drivers. KOSPI was subdued after the BoK charge resolution wherein the central financial institution saved charges unchanged as anticipated, though 6 out of the 7 board members noticed the necessity to hold the door open for yet one more charge hike. Hold Seng and Shanghai Comp. had been pressured with underperformance in Hong Kong after the benchmark index slipped beneath the 19,000 stage, whereas the mainland was lacklustre amid current US-China frictions.

High Asian Information

- Chinese language corporations reportedly swap auditors to keep away from US delisting threat, in keeping with FT.

- USTR Tai is reportedly to fulfill with Taiwan’s minister in command of the Workplace of Commerce Negotiations.

- BoK maintained its base charge at 3.5%, as anticipated, by means of a unanimous resolution though six board members noticed the necessity to hold the door open for yet one more charge hike. BoK assertion famous financial progress is to stay weak for a while and inflation will possible fall significantly earlier than rebounding barely for the remainder of the 12 months, whereas it said uncertainty is excessive over the Chinese language financial system and IT sector, in addition to lowered its 2023 GDP progress forecast to 1.4% from 1.6%. Moreover, BoK Governor Rhee stated core inflation just isn’t easing as a lot as board members had anticipated and that board members share the opinion that it’s untimely to speak a couple of charge reduce this 12 months with uncertainty increased over relating to whether or not inflation will strategy the two% goal earlier than year-end.

- RBNZ Governor Orr stated charges are restrictive and effectively above impartial, whereas he added that financial progress and inflation are weaker than anticipated though they’ll change the evaluation if wanted as new knowledge emerges, in keeping with Reuters.

- BoJ Governor Ueda says we’re starting to see good indicators within the financial system however nonetheless a ways to stably and sustainably hit inflation goal; BoJ will patiently maintain simple financial coverage.

- Japan raises Might total financial view for first time since July 2022 and says financial system is recovering reasonably.

European bourses are combined after preliminary stress on a detrimental German GDP revision, DAX 40 -0.2%; although, tech is the standout outperformer post-NVDA, with Euro Stoxx 50 +0.3% as such. Stateside, the NQ +1.9% and ES +0.7% are firmer, given Nvidia, whereas the RTY and YM reside in detrimental territory amid broader market concern over the debt ceiling and after Fitch’s replace. Nvidia (NVDA) Q1 23 (USD): Adj. EPS 1.09 (exp. 0.92), income 7.19bln (exp. 6.52bln). Q2 23 income view 11bln (+/- 2%) (exp. 7.18bln). CFO stated that the information centre income rise within the quarter is led by rising demand for generative AI and huge language fashions utilizing GPUs. +24% in pre-market commerce. Swiss authorities to begin session on liquidity backstop of all systemically necessary banks, in keeping with the Finance Ministry; SNB’s Maechler says Credit score Suisse (CSGN SW) disaster was one in every of confidence.

High European Information

- ECB’s Vasle stated the ECB should nonetheless elevate charges additional and inflation is changing into more and more cussed.

- Riksbank’s Thedeen says the SEKs stage is worrying.

- UK’s Ofgem units the vitality worth cap at GBP 2074 for dual-fuel households (prev. 3280), for July-September; the cap represents a discount QQ and a discount in how a lot prospects pays on their payments.

- Transport exercise returns to regular in Suez Canal after a malfunctioning ship was towed away, in keeping with Two Canal.

FX

- Greenback stays dominant as US debt ceiling talks proceed productively, DXY tops 104.000 and probes Fib at 104.090.

- Kiwi descends additional as RBNZ Governor Orr underscores steerage indicating no additional tightening, NZD/USD hovers underneath 0.6100.

- Euro undermined by surprising detrimental German Q1 GDP print, EUR/USD fades from simply above 1.0750 and EUR/GBP retreats by means of sub-0.8700 10 DMA.

- Sterling rebounds in the direction of 1.2400 vs Buck as Gilts reverse sharply from post-UK inflation correction lows.

- Yen hits new y-t-d trough, however stays afloat of huge possibility limitations seen at 140.00 in opposition to Buck

- PBoC set USD/CNY mid-point at 7.0529 vs exp. 7.0515 (prev. 7.0560)

- Turkey requested banks to purchase greenback debt to help default swaps, in keeping with Bloomberg.

Mounted Earnings

- Gilts markedly underperform amidst reversion towards post-UK inflation knowledge lows inside a 96.24-95.10 vary.

- Bunds and T-notes retreat in sympathy between 133.93-56 and 113-12+/00 bounds, the previous regardless of Q1 German GDP contraction and the latter forward of US IJC, GDP, Fed audio system and seven 12 months public sale.

- BTPs resilient and solely slightly below par within the wake of well-received Italian end-of-month provide.

Commodities

- Crude benchmarks are softer intraday, with WTI & Brent July underneath USD 73.50 and USD 77.50/bbl respectively after mushy German knowledge and remarks from Novak forward of subsequent week’s OPEC+ confab; most lately, the benchmarks are nearer to USD 73.00/bbl and USD 77.00/bbl.

- On this, ING writes that “There’s a massive speculative gross brief out there and they’re going to possible be hesitant to hold an excessive amount of threat into the OPEC+ assembly scheduled for 4 June”.

- Spot gold is deriving help from the broader macro tone, ex-tech, although is but to see any actual haven bid regardless of the Fitch replace and because the X-date attracts nearer as updates on progress this morning are more-encouraging, total.

- Base metals combined with LME Copper nonetheless underneath USD 8k/T whereas tin was initially bolstered after the Wa area reiterated its mining ban.

- Russian Deputy PM Novak says don’t see new steps on the June 4th OPEC+ assembly and sees Brent crude above USD 80/bbl by year-end.

- Chevron (CVX) launched the sale of tis oil and fuel belongings in Congo which may elevate as much as USD 1.5bln, in keeping with Reuters sources.

Debt Ceiling Headlines

- US Home Speaker McCarthy stated he believes they’ll get again to a 2022 spending stage and has all the time thought that they may get a deal in a day, whereas he additionally said there shouldn’t be any worry in markets and negotiations have made some progress. McCarthy additionally famous that quite a few points stay unresolved however added that issues are higher than they had been the prior day, whereas he’ll keep in Washington DC this weekend and stated they may get a debt settlement in precept this weekend, in keeping with Reuters.

- US Home Majority Chief Scalise stated the weekend recess will start on Thursday as deliberate, whereas debt ceiling talks will proceed and lawmakers ought to be able to return in case of a deal. Scalise additionally said that members will get 24 hours’ discover that they should return if an settlement is reached and members will get 72 hours to learn any debt ceiling invoice, in keeping with Reuters.

- US Home Republican management reportedly feels superb concerning the state of the debt restrict negotiations after a number of days of little progress, in keeping with Punchbowl’s Jake Sherman.

- US Home Democratic chief Jeffries demanded that the size of spending caps match the size of the debt restrict enhance, in keeping with a Bloomberg reporter.

- Fitch positioned the US AAA sovereign score on Ranking Watch Damaging which displays the elevated political partisanship that’s hindering a decision to boost or droop the debt restrict, whereas it nonetheless expects a decision to the debt restrict earlier than the X-date however believes dangers have risen that the debt restrict is not going to be raised or suspended previous to the X-date. Fitch added that it could anticipate the US nation ceiling to stay at AAA even within the state of affairs of a debt default and believes a failure to make full and well timed funds on debt securities is much less possible than reaching the X-date and is a really low likelihood occasion, in keeping with Reuters.

- White Home stated the Fitch report reinforces the necessity for Congress to rapidly go a bipartisan settlement to keep away from a debt default, whereas the US Treasury stated brinkmanship over the debt restrict does severe hurt to companies and American households, raises short-term borrowing prices for taxpayers and threatens the credit standing of the US.

- Many throughout the US Home Republican Management anticipate a deal to be finalised by the weekend, by way of Punchbowl; if a deal got here collectively on Thursday, it could take round two days to transform this into legislative textual content, implying a ultimate vote as quickly as Tuesday. Albeit, Punchbowl writes “it appears very doable that Congress received’t be capable of carry the debt restrict till subsequent weekend, which is June 3-4”.

Geopolitics

- EU is reportedly discussing sending earnings from EUR 196.6bln of frozen Russian belongings to Ukraine, in keeping with FT.

- Twitter sources famous air raid sirens in Kyiv and that Shahed drones had been launched in the direction of northern and southern Ukraine.

- A whole bunch of 1000’s of South Korean artillery rounds are on their solution to Ukraine by way of the US, in keeping with WSJ sources.

- Russian and Belarus Defence Ministers have signed a doc on the deployment of tactical nuclear weapons in Belarus, by way of Tass; Russia’s Shoigu says West is waging undeclared battle in opposition to Russia and Belarus, in keeping with RIA; Defence Minister Shoigu says Russia are to manage nuclear weapons in Belarus, in keeping with IFX.

- China Commerce Minister Wang will meet US Commerce Secretary Raimondo, in keeping with Reuters citing the Chinese language Commerce Ministry

- Japan Defence Ministry says Japan scrambled jets after recognizing Russian info gathering aircrafts over pacific ocean, sea of Japan on Thursday.

US Occasion Calendar

- 08:30: Might Preliminary Jobless Claims, est. 245,000, prior 242,000

- Might Persevering with Claims, est. 1.8m, prior 1.8m

- 08:30: 1Q GDP Annualized QoQ, est. 1.1%, prior 1.1%

- 1Q Private Consumption, est. 3.7%, prior 3.7%

- 1Q GDP Value Index, est. 4.0%, prior 4.0%

- 1Q PCE Core QoQ, est. 4.9%, prior 4.9%

- 08:30: April Chicago Fed Nat Exercise Index, est. -0.20, prior -0.19

- 10:00: April Pending Dwelling Gross sales YoY, est. -20.1%, prior -23.3%

- 10:00: April Pending Dwelling Gross sales (MoM), est. 1.0%, prior -5.2%

- 11:00: Might Kansas Metropolis Fed Manf. Exercise, est. -9, prior -10

Central Financial institution Audio system

- 09:50: Fed’s Barkin Speaks at Southwest Virginia Financial Discussion board

- 10:30: Fed’s Collins Speaks at Group School of Rhode Island

DB’s Jim Reid concludes the in a single day wrap

Given it’s our AI week, it’s acceptable that one of many world’s largest chipmakers Nvidia reported earnings final night time, which included an outlook far above expectations due to demand for AI processers. They stated that income within the three months ending July was anticipated to be $11bn, which was effectively above analysts’ estimates for $7.18bn, and their shares had been up by round 25% in after-hours buying and selling. That’s given an enormous enhance to different chipmakers too, and futures for the NASDAQ 100 are up by +1.39% this morning. As an illustration in Tokyo, shares within the tools provider Advantest are up +15.58% this morning, while the memory-chip maker SK Hynix is up +4.50% in Seoul.

Though AI may show to be a turning level, elsewhere truly noticed markets droop once more yesterday as fears ramped up on a number of fronts. The largest concern proper now’s the US debt ceiling, the place there’s nonetheless no signal of a decision, regardless that we could be as little as per week away from the Treasury being unable to pay its payments. On prime of that, there was a really sturdy UK inflation print, which introduced again fears that extra persistent inflation was nonetheless on the playing cards and central banks would wish to maintain mountain climbing charges to cope with that. And the opposite knowledge from the final 24 hours was additionally fairly weak, such because the Ifo’s enterprise local weather indicator from Germany that noticed its largest month-to-month decline since September. All this led to a different mixed bond-equity selloff, with the S&P 500 down -0.73%, while yields on 10yr Treasuries had been up +5.0bps to three.74%.

For now at the least, the main target continues to be very a lot on the debt ceiling, the place there are a number of indicators of rising market stress across the X-date. When it comes to the most recent information, there wasn’t something notably promising, with Speaker McCarthy saying to reporters that “there are a variety of locations the place we’re nonetheless far aside”. He famous afterward that he thinks “we have now time to get an settlement”, and stated it may occur over the weekend, however so far there haven’t been any tangible indicators of progress. After the US shut, we then heard from the credit standing company Fitch that they’d positioned the US’ AAA score on “Ranking Watch Damaging”. While their base case was {that a} deal could be reached, they stated that the transfer was all the way down to “elevated political partisanship” and mirrored rising dangers that “the federal government may start to overlook funds on a few of its obligations.”

The dearth of any settlement (and even indicators of 1) has meant that market stress across the X-date has solely continued to rise, with front-end T-bills across the debt ceiling now yielding effectively above 6%. As an illustration, the invoice that matures on June 1 noticed its yield surge by +111bps yesterday to six.84%, and the invoice maturing on June 6 is now at 6.68% (+65bps yesterday). The results of which might be more and more being felt additional out the curve as effectively, with the 3-month yield (+10.1bps) closing at a post-2001 excessive yesterday of 5.33%.

These bond losses pushed by the debt ceiling had been additionally interacting with a really sturdy upside shock in UK inflation earlier within the day, which confirmed headline CPI at +8.7% in April (vs. +8.2% anticipated). That was above each economist’s expectation on Bloomberg, in addition to the +8.4% projection from the BoE a few weeks in the past. Moreover, core CPI rose to its highest stage since 1992, at +6.8% (vs. +6.2% anticipated). The studying added to fears that inflation was changing into entrenched, which led traders to quickly dial up their expectations for charge hikes from the BoE. As an illustration, additional 25bp hikes at the moment are totally priced in for the subsequent two conferences in June and August, while terminal charge pricing has additionally surged, with the height charge seen by the December assembly standing 92bps above present ranges.

While it was simply the UK that had a powerful inflation print yesterday, traders responded by dialling up the probabilities of charge hikes extra broadly. And people strikes then obtained additional momentum due to a speech from Fed Governor Waller, who signalled a transparent openness to a different hike in June, saying that “I don’t help stopping charge hikes except we get clear proof that inflation is transferring down in the direction of our 2 % goal.” He framed the choices round mountain climbing, skipping, or pausing, suggesting that there was thought being given to the thought of skipping a hike in June forward of one other hike in July. Atlanta Fed President Bostic later reiterated his choice for each a close to time period pause and for no charge cuts till “effectively into 2024.” In response, traders dialled up the probabilities of a hike by July, with futures now placing the prospect at 66% this morning, which exhibits how that is now being critically thought-about by market members. Trying additional out, the speed anticipated by the December assembly additionally hit a post-SVB excessive of 4.83% by the shut yesterday, and this morning that’s risen additional to 4.86%, which simply exhibits how traders are more and more pricing out the probabilities of charge cuts this 12 months.

With one other upside shock on inflation and hawkish rhetoric from officers, sovereign bonds bought off on either side of the Atlantic. UK gilts had been on the epicentre of this, with the 2yr gilt yield ending the session up by an enormous +23.7bps, taking it as much as its highest stage since September 27, simply after the mini-budget that triggered market turmoil. Likewise, the 10yr yield was up +5.6bps to its highest stage since October. Within the US, yields on 10yr Treasuries had been up +5.0bps to three.74%, which is their highest stage because the SVB collapse, and in Europe yields on 10yr bunds (+0.3bps), OATs (+0.9bps) and BTPs (+1.7bps) all moved increased as effectively. In a single day, 10yr Treasury yields have seen an extra +0.8bps enhance to three.75%.

The deteriorating international backdrop additionally led to a nasty day for equities, with the S&P 500 (-0.73%) dropping floor for a second day operating amidst broad-based declines. Over in Europe the losses had been much more extreme, with the STOXX 600 (-1.81%) seeing its worst every day efficiency since March 15 on the peak of the market turmoil over Credit score Suisse, which took the index again to a 7-week low. On a sectoral foundation, the largest outperformer was vitality due to an extra rise in oil costs, with Brent crude (+1.98%) closing at a 3-week excessive of $78.36/bbl.

One other occasion yesterday had been the most recent Fed minutes from the assembly on Might 2-3, however they weren’t a very market-moving occasion. They confirmed that the committee members had been changing into extra open to a pause in charge hikes, and it stated that “Many members centered on the necessity to retain optionality” transferring ahead. Some members famous that because the “progress in returning inflation to 2% may proceed to be unacceptably sluggish, further coverage firming would possible be warranted at future conferences.” However the counter was that if there have been a medium-term financial slowdown there wouldn’t be the necessity for additional tightening. There was additionally a word that “that knowledge by means of March indicated that declines in inflation, notably for measures of core inflation, had been slower than that they had anticipated”, which correlates to Fed audio system changing into extra hawkish in current weeks.

In a single day in Asia, the selloff has principally continued, with losses for the Hold Seng (-2.07%), the Shanghai Comp (-0.66%), the CSI 300 (-0.49%), and the KOSPI (-0.52%). The principle exception is the Nikkei, which has posted a +0.50% advance. And searching ahead, there are indicators that markets at the moment are starting to stabilise, with futures on the S&P 500 up +0.38% this morning, having been helped by the sturdy Nvidia earnings final night time.

On the information facet, the primary launch yesterday except for the UK CPI print was the Ifo’s enterprise local weather indicator from Germany. That got here in at 91.7 in Might (vs. 93.0 anticipated), and marked an finish to six consecutive month-to-month features in that indicator. The expectations studying fell to 88.6 (vs. 91.6 anticipated), ending a run of seven consecutive features, and the present evaluation studying fell to 94.8 (vs. 94.7 anticipated). While the discharge is just one indicator, it provides to the sample throughout Europe in current months whereby we’re not seeing the massive upside surprises from Q1, and if something the releases have been extra on the draw back of late.

Lastly within the political sphere, there was one other announcement within the 2024 presidential race yesterday as Florida Governor Ron DeSantis formally confirmed he could be a candidate. In line with FiveThirtyEight’s polling common for the Republican nomination, DeSantis is presently in second place behind former President Trump. Nevertheless, Trump’s lead has widened considerably over the past couple of months, and Trump presently stands at 54.3%, with DeSantis a way behind on 20.6%, after which former Vice President Pence (who hasn’t but declared) on 5.3%. The primary primaries received’t truly be till 2024, however based mostly on previous cycles we are able to anticipate the sector to return more and more into view over the summer season as the assorted candidates search to coalesce public help, elevate funds and win key endorsements beforehand.

To the day forward now, and knowledge releases from the US embody the weekly preliminary jobless claims, the second estimate of Q1 GDP, pending residence gross sales for April, and the Kansas Metropolis Fed’s manufacturing index for Might. Central financial institution audio system embody the Fed’s Barkin and Collins, ECB Vice President de Guindos and the ECB’s Nagel, Villeroy, Centeno and De Cos, together with the BoE’s Haskel.

Tyler Durden

Thu, 05/25/2023 – 08:11